For many Veterans and active-duty military families, buying a home can feel overwhelming in today’s market. Rising interest rates, higher home prices, and the assumption that a large amount of savings is required often cause buyers to put their plans on hold before even exploring their options.

What surprises many service members is that their VA home loan benefit may offer advantages that significantly reduce the upfront financial burden of purchasing a home.

After years of service, many Veterans still don’t fully understand how powerful this benefit can be or how it may help them achieve homeownership sooner than expected.

The VA Loan Program Was Designed To Help Veterans Become Homeowners

The VA home loan program was created to provide qualifying Veterans, active-duty military members, and certain surviving spouses with a more accessible path to homeownership.

While conventional loans often require substantial cash reserves, mortgage insurance, and stricter lending requirements, VA loans were designed with flexibility and affordability in mind.

Yet many eligible buyers mistakenly believe the process is similar to a standard conventional loan.

You May Not Need a Down Payment

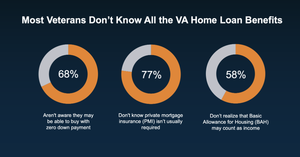

One of the most valuable features of a VA loan is the potential ability to purchase a home without a down payment.

Many buyers assume they need to save tens of thousands of dollars before they can even begin shopping for a home. That belief alone keeps some military families renting longer than necessary.

Depending on eligibility and lender requirements, qualified VA buyers may be able to finance 100% of the purchase price, allowing them to preserve savings for moving expenses, furnishings, repairs, or emergency reserves.

For military families relocating throughout East County San Diego or communities like Jamul, this can make a major difference in affordability.

VA Loans Often Reduce Out-Of-Pocket Costs

Closing costs are another area where Veterans are frequently misinformed.

Many buyers expect they’ll need a large amount of cash on hand to finalize their purchase, but VA loans place restrictions on certain fees and costs charged to buyers. In some situations, sellers may also contribute toward allowable closing expenses during negotiations.

This can help reduce the amount needed at closing and create a smoother transition into homeownership.

No Monthly PMI Is a Huge Advantage

With many conventional loan programs, buyers who put less than 20% down are typically required to pay private mortgage insurance, commonly referred to as PMI.

That additional monthly expense can add hundreds of dollars to a mortgage payment every single month.

VA loans are different.

Eligible VA buyers can often avoid monthly PMI entirely, even when purchasing with little or no money down. Over time, that savings can add up significantly and improve long-term affordability.

Military Housing Allowances May Strengthen Purchasing Power

For active-duty military members and some reservists, allowances such as BAH (Basic Allowance for Housing) and BAS (Basic Allowance for Subsistence) may also be considered as part of qualifying income.

Because these benefits are generally non-taxable, they can positively impact purchasing power and help some buyers qualify for more than they initially expected.

This is one of the most commonly overlooked aspects of VA financing.

Why This Matters in Today’s Housing Market

In a market where affordability continues to challenge buyers across California, understanding the benefits available through a VA loan can be incredibly important.

The opportunity for:

- No down payment

- Reduced upfront expenses

- No monthly PMI

- Flexible qualification standards

can help military families create a path toward homeownership that may feel more achievable than they originally thought.

Work With Professionals Familiar With VA Financing

Not every lender or real estate professional has experience navigating VA loans. Working with knowledgeable professionals who understand the process can help Veterans better understand their options, monthly costs, and overall purchasing strategy.

At The Svelling Group, Zachary and Rochelle Svelling are proud to support military families throughout East County San Diego with personalized guidance and white-glove service designed to help every move feel seamless.

Bottom Line

Many Veterans qualify for far more home-buying advantages than they realize.

If you’ve been delaying your plans because you assumed you needed a large down payment or expensive monthly mortgage insurance, it may be worth exploring your VA loan benefit more closely.

The information you don’t know could be the very thing that helps make homeownership possible sooner than expected.

Check out this article next